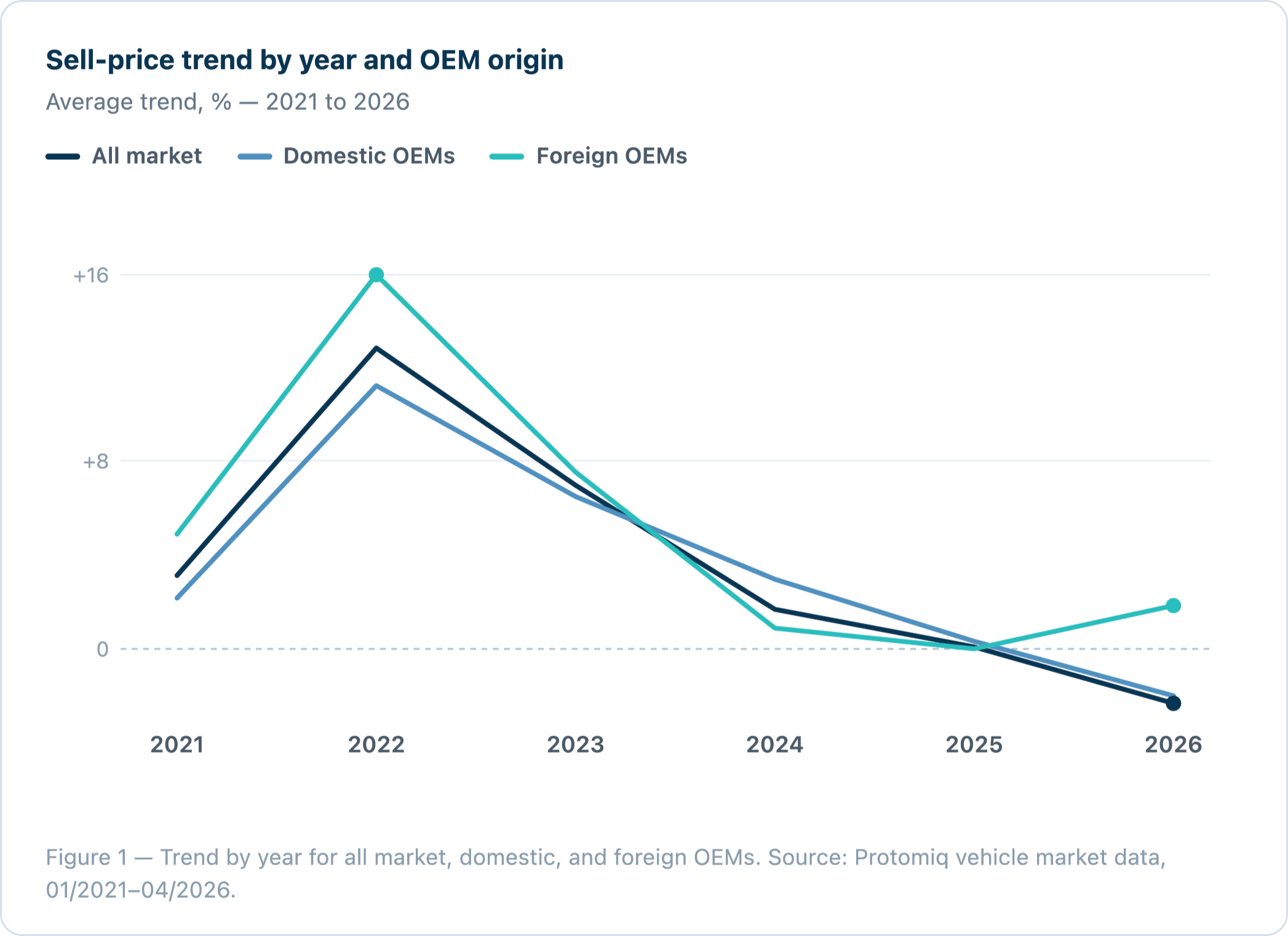

2022 was the peak, 2025 was the soft patch, 2026 is fragmented

Across several cuts of the data, 2022 showed unusually strong positive movement. By 2025, several metrics had softened sharply. In 2026, some categories recovered while others remained weak. Regionally, 2022 was strong across every major region; 2025 was weak, with the West and Northeast turning negative; and 2026 returned to positive sell-price movement across major regions — while MSRP discount pressure remained negative.

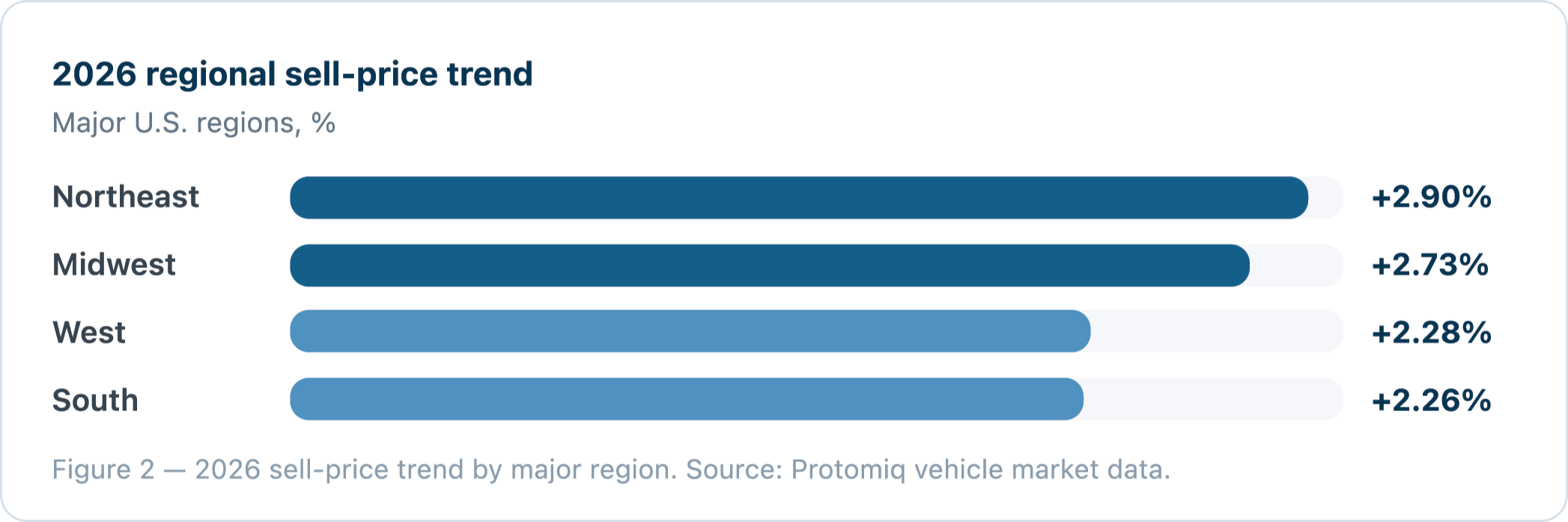

Regional market fragmentation: where 2026 strength is showing up

The 2026 regional data shows positive sell-price movement across major regions, but the degree of discount pressure varies. The Northeast leads at +2.90%, followed closely by the Midwest at +2.73%; the West (+2.28%) and South (+2.26%) trail — and the West carried the most negative 2026 MSRP discount pressure among the major regions at −2.64%.

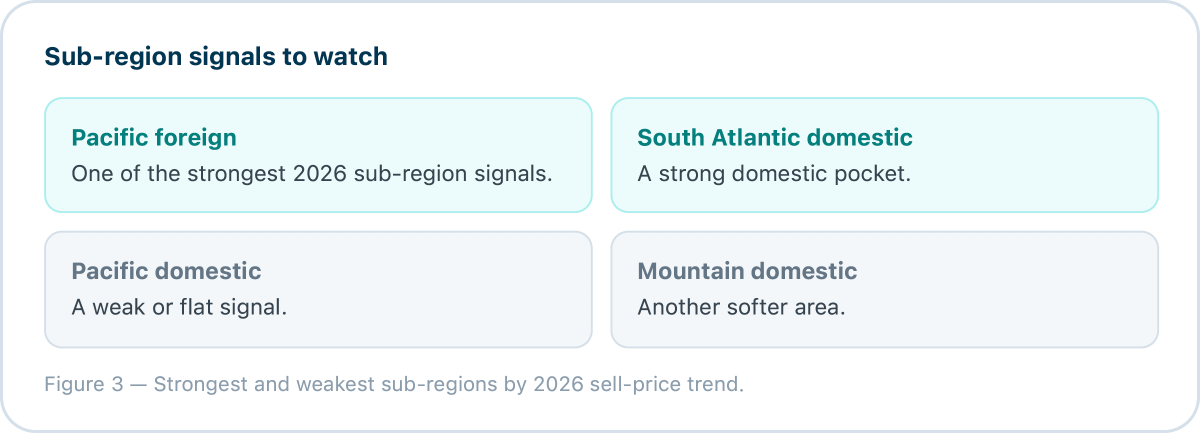

In 2026, foreign OEMs were stronger in the West, domestic OEMs were stronger in the Midwest and South, and the Northeast was closer — with foreign slightly stronger.

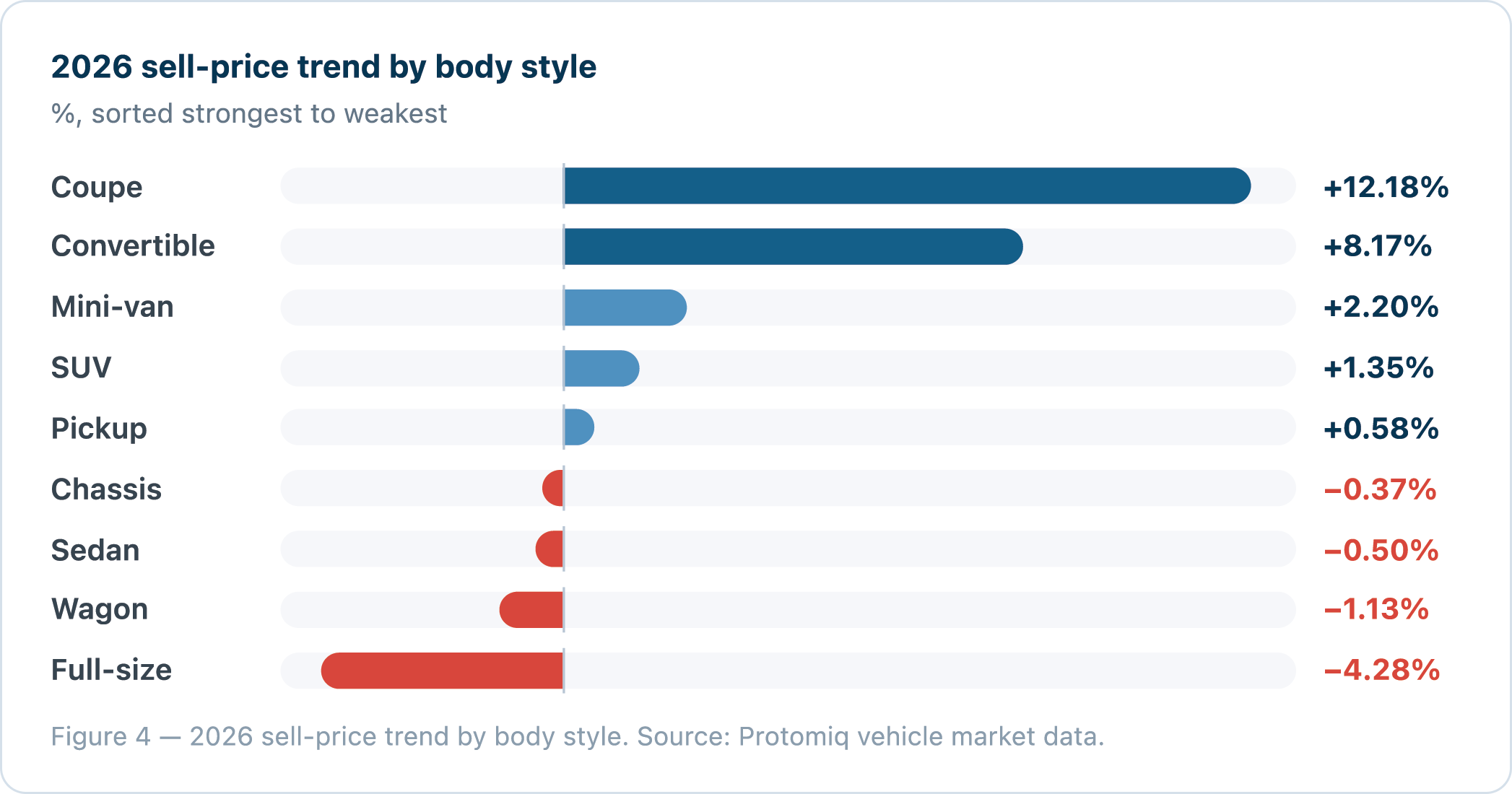

Body style winners and risk pockets

Body style is one of the clearest separators between opportunity and risk. The strongest 2026 sell-price trends belong to coupes (+12.18%) and convertibles (+8.17%), with mini-vans (+2.20%), SUVs (+1.35%), and pickups (+0.58%) modestly positive. The weaker categories: full-size (−4.28%), wagon (−1.13%), sedan (−0.50%), and chassis (−0.37%).

SUVs and pickups remain core dealership inventory, but their 2026 trends are only modestly positive. The data does not support blanket aggressive bidding on those categories. “Core inventory is not automatically low-risk.”

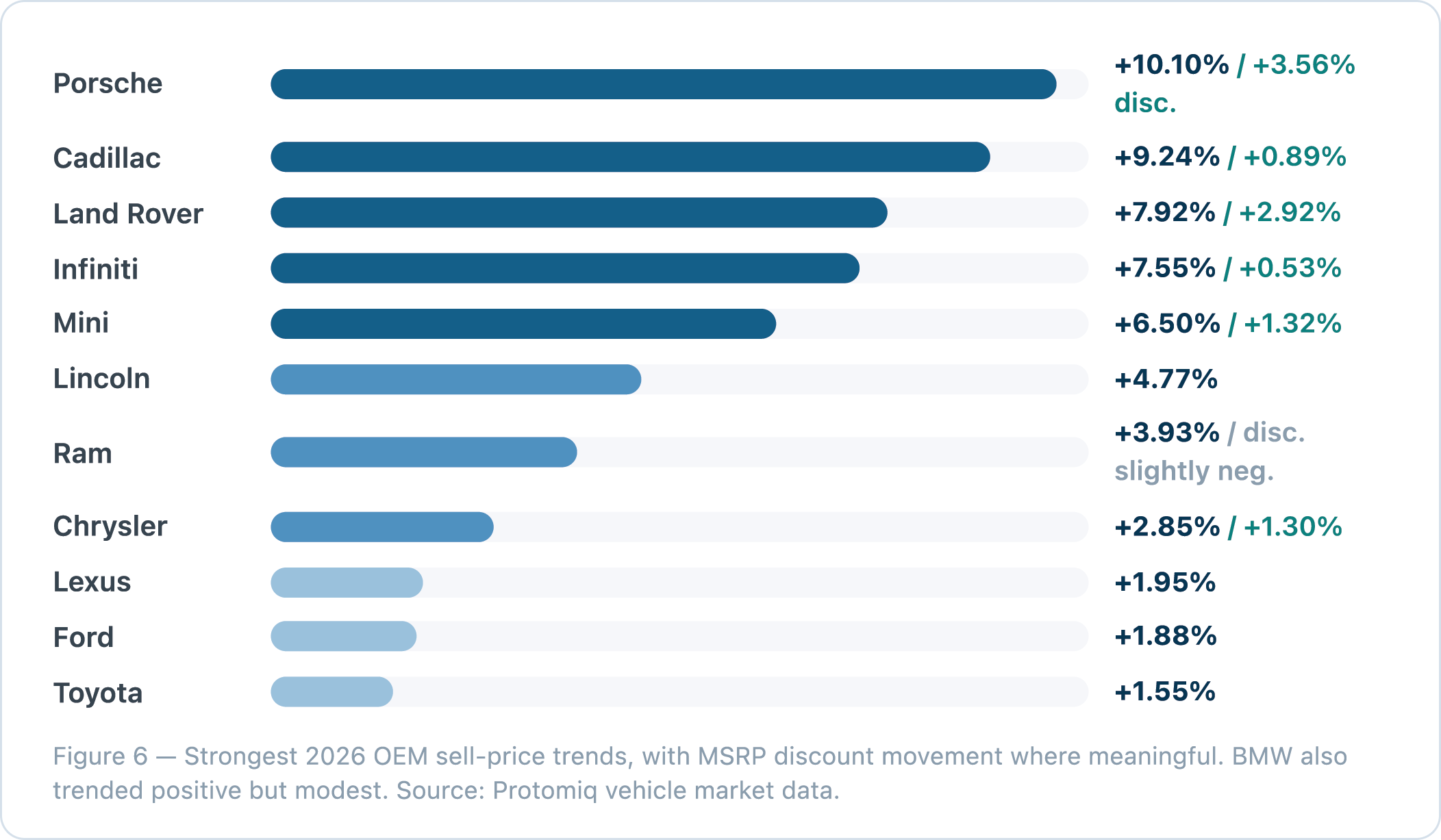

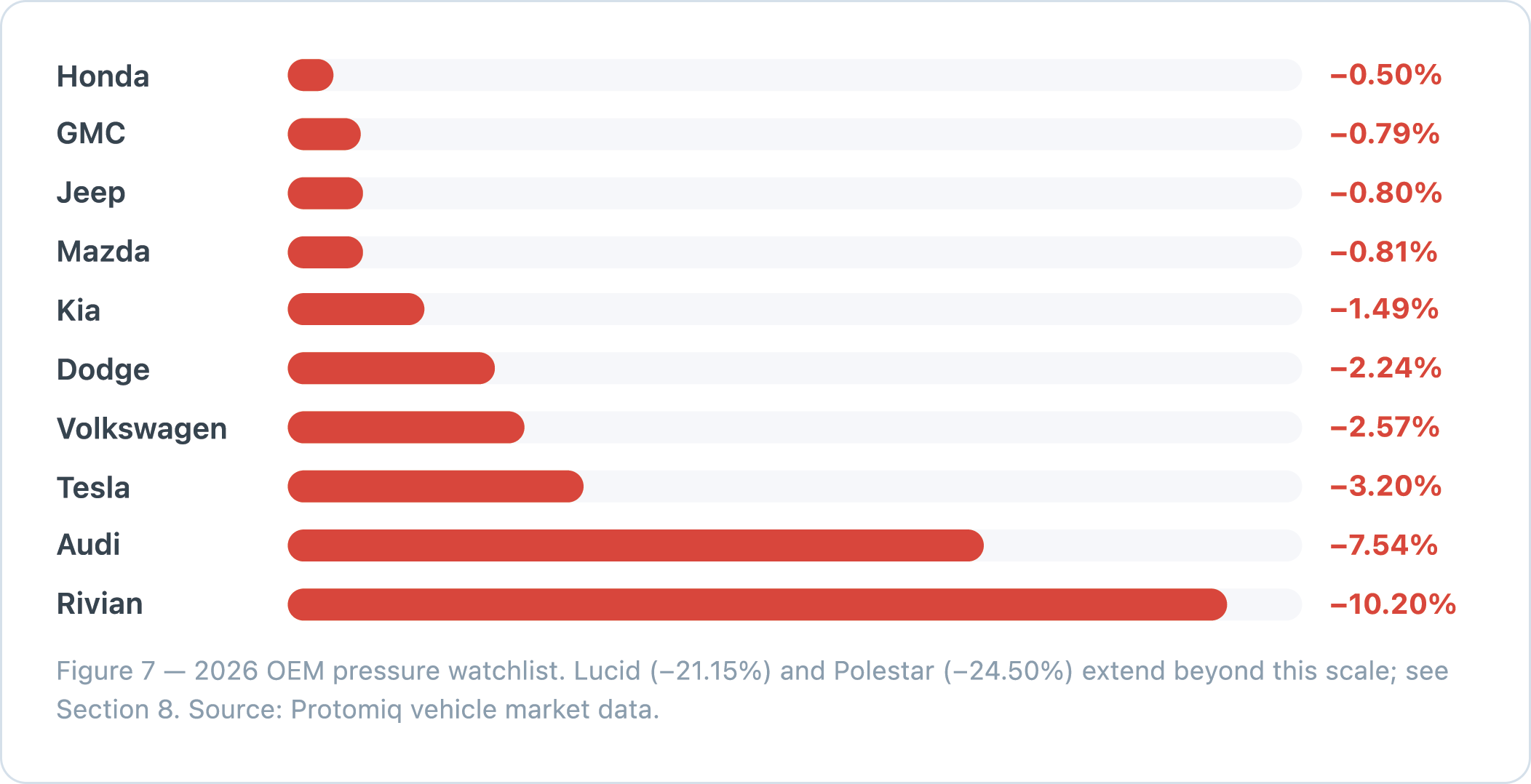

The market is being decided brand by brand

The OEM readout shows that 2026 strength is highly uneven. Some brands show both positive sell-price movement and positive discount movement, while others remain under meaningful pressure.

Stronger 2026 OEM signals

Weaker 2026 OEM signals

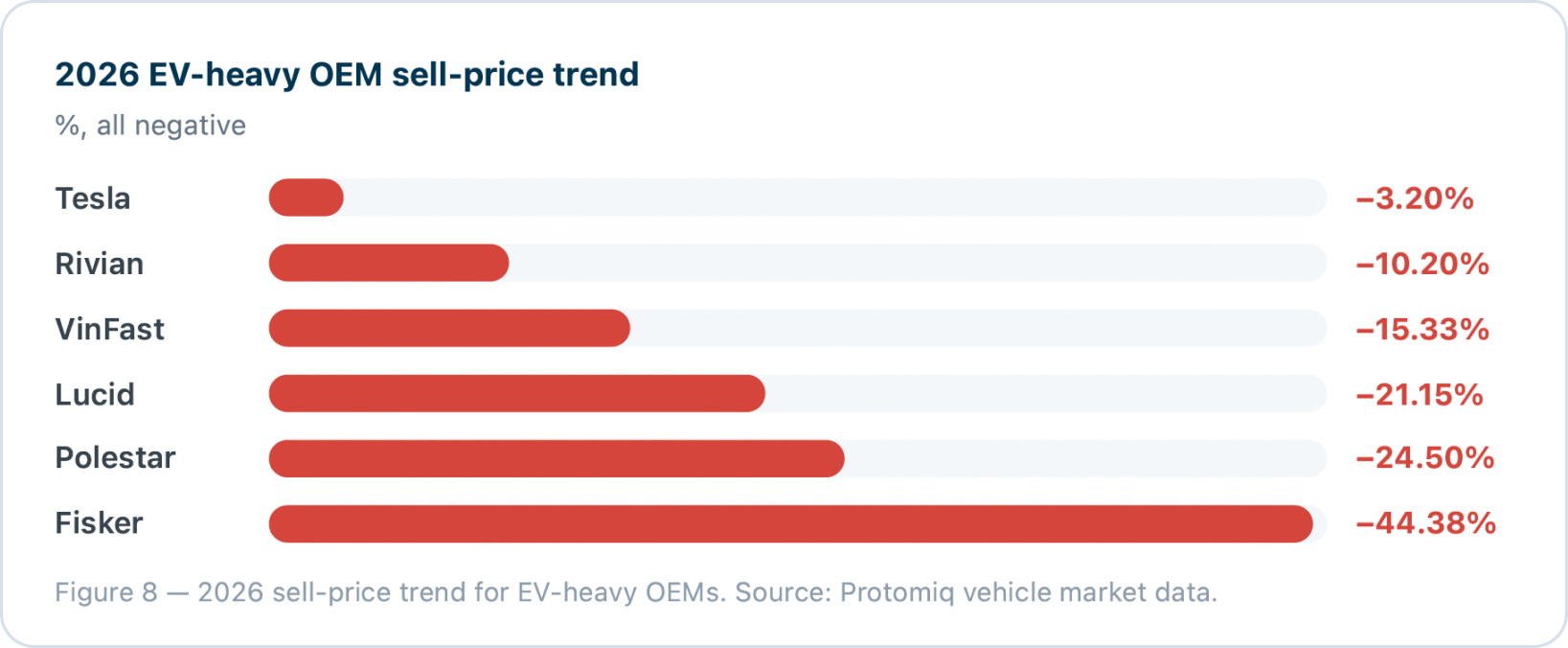

EV pressure: the clearest risk category

The OEM data shows consistent pressure among EV-heavy and newer EV brands. Every brand in this group posted a negative 2026 sell-price trend — several of them steeply negative.

Several forces compound this pressure: EV incentive changes, new-EV price cuts, steep used-EV depreciation, consumer concerns around range and charging, battery condition and technology obsolescence, and a wave of lease returns adding used EV supply.